Medical claim trends highlight value of stop-loss partnership

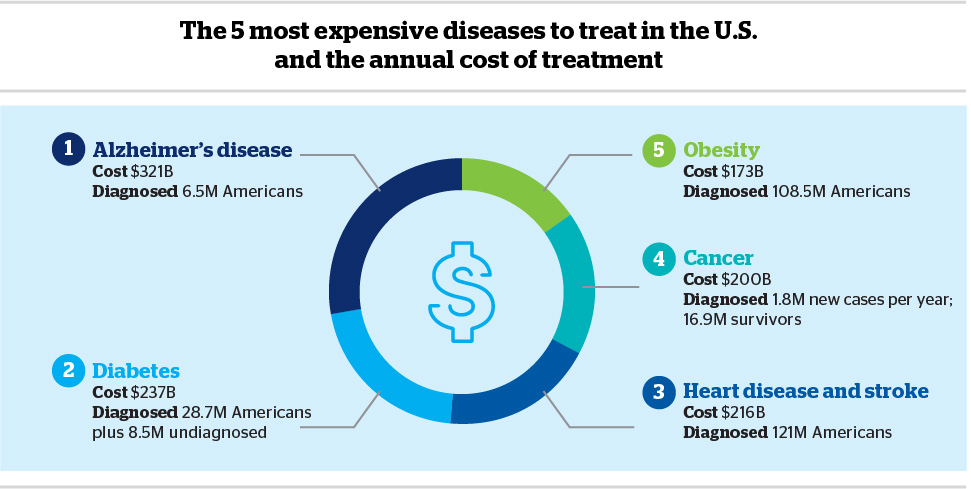

Tara Krauss | Head of Accident & Health, QBE North America Self-funding medical benefits continues to be an important cost-containment strategy for employers, yet it’s the insights provided around claims trends that are providing transparency into high health plan costs. Among these trends are a greater incidence of neoplasms – abnormal tissue development that can be cancerous – and the emergence of expensive specialty drugs. Medical stop-loss coverage has become an increasingly useful financial risk transfer mechanism for employers that elect to self-fund, and working with the right stop-loss partner offers numerous advantages. QBE North America’s 2024 Accident & Health Market Report highlights trends in stop-loss reimbursements and provides learnings for self-funded employers. The market report notes that the frequency of medical stop-loss claims above an attachment point of $200,000 for 10,000 covered employees grew by 39% in 2023 from the prior years. Among all stop-loss claim reimbursements in 2023, the most frequent claims were those involving neoplasms – representing 41% of all stop-loss reimbursements. Claim severity was led by premature births, with an average reimbursement of $488,000. By primary diagnosis, QBE found the leading stop-loss claim reimbursements, which include medical and drug claims across varying deductible levels from $100,000 to $1 million, were: Another key finding of QBE’s latest market report is that specialty drugs have increased treatment costs for certain types of cancers. Cell and gene therapies are leading the list of new pharmaceuticals, and the U.S. Food and Drug Administration approved five new gene therapies in 2023 alone. That number is certain to rise. LabCompare.com indicates at least 600 developers in the United States worked on cell and gene therapy projects in 2023, with 2,000 of them entering clinical trials. GlobalData estimates the worldwide sales for cell and gene therapies will reach $80 billion by 2029. The number of new specialty drugs and cancer therapies is only part of the equation. Cost is another, and that is growing at a concerning pace. The median annual list price of a new drug in 2023 was $300,000, a 35% increase from the median a year earlier. Why are specialty pharma costs spiraling out of control? There are several reasons. Among them are inadequate regulatory oversight, lack of transparency in drug pricing models, and the settings in which the drugs are administered. About half of specialty drugs are dispensed through a health plan’s pharmacy benefit and can be self-administered orally or at home by the patient. Utilization and cost of these can usually be managed by a prescription benefit manager (PBM) through formularies or prior authorization requirements. The other half of specialty drugs, however, bypass these cost controls because they are administered in a physician’s office or healthcare facility, and the treatment cost is billed to a plan’s medical benefit. PBMs play a key role in the cost of pharma benefits, and 80% of the healthcare market is controlled by three players. PBMs can provide valuable administrative and claims services, but they also negotiate drug prices and rebates with manufacturers in a system that is anything but transparent. That makes it difficult, if not impossible, for employers to see what’s driving their costs in pharmacy benefits. Federal legislation is pending that would increase transparency and provide more regulation of PBMs. Among QBE’s other findings in the market report is a sharp rise in the claim frequency of mental illness. Frequency for this category of claim has increased steeply since 2021 and is driven largely by substance abuse, depression and anxiety. Stop-loss claim trends point to a sobering reality: the U.S. healthcare system is more focused on “sick care” than wellness. Financial incentives, from providers to pharmaceutical companies, are geared to treating sickness rather than improving overall health. Among the five most expensive diseases to treat in the United States, all can benefit from a focus on the profound impact that lifestyle factors, including nutrition, environmental toxins and stress, have on our health. New cases are diagnosed annually for all of these diseases: Alzheimer’s disease, diabetes, heart disease and stroke, cancer, and obesity. Spending on healthcare is not decreasing. In 2023, the United States was forecast to spend nearly $4.7 trillion on healthcare, nearly one-fifth of the nation’s economy. For employers, healthcare costs continue to rise, year after year. This is not a sustainable pattern, and it requires a shift in our approach to healthcare for change to occur. The principal focus should be on preventing or improving underlying health conditions, rather than the far-costlier approach of treating the consequences. Obesity, for example, is a precursor to many other chronic diseases, including cancer. There is optimism, however, as younger generations of consumers are spending more on health and wellness. Employer groups should consider this movement toward preventive care and encourage it through thoughtful benefit and wellness programs. A proven method of self-funding various kinds of risks is captive insurance. Captive entities have been used for decades as tools for self-insuring and mitigating risk. A growing number of health plan sponsors are seeing value in placing medical stop-loss coverage within captives. This aligns well with captives’ long history of success in controlling the cost of property and liability risks and is complementary to the property and liability coverage given its short-tail nature. Medical stop-loss captives, either as single-parent or group captives, are a creative solution to contain the rising costs of commercial health plans. QBE North America works with captive owners to develop cost-effective medical stop-loss programs. Whether through a captive or other risk transfer mechanism, self-funding benefits offers a variety of advantages, including medical cost containment, greater flexibility to meet the needs of employees and their dependents, and more insight into health claims. With knowledge there is power. Knowing high-cost facility usage or high-cost pharmacy spend, for example, can empower an employer group to institute meaningful plan and point solution changes that can improve the employee experience, value of care and the bottom line for the health plan. About two-thirds of U.S. employers self-fund healthcare benefits, and because of the meaningful change a self-funded plan can provide, interest in self-funding is increasing for smaller employers with fewer than 250 covered lives. Medical stop-loss is a critical piece of a self-funding strategy, and working with the right stop-loss partner can provide self-funded employer health plans several advantages over fully insured plans. These include: Financial certainty. Stop-loss coverage enables employers to fund unexpectedly large claims and obtain financial certainty for plan expenses. Funding flexibility. With quality stop-loss coverage, self-funded employers have flexible options for specific deductibles and competitive attachment points for aggregate stop-loss protection. Expertise. A strong stop-loss partner can offer self-funded employers technical and clinical expertise, to answer questions and understand the complexities of care. Insight. A good stop-loss partner acts as a second set of eyes on claims, enabling employers to better understand frequency and severity trends in their plans and take proactive action to optimize cost containment. For example, are pharmaceutical costs about average or out of line with expected expenses? Stop-loss claims managers can share this and other data with self-funded employers. Education. A major burden on employers is educating plan members about health and wellness, as well as helping them to choose the best care. An experienced stop-loss partner can assist employers in increasing plan members’ awareness of specific health trends, so they can make better-informed decisions about their health and seek appropriate care. For more information on QBE’s Accident & Health solutions, including medical stop-loss and captive options, please visit https://www.qbe.com/us/ah. Tara Krauss is the Head of Accident & Health at QBE North America.

Sick care vs. healthcare?

Stop-loss in captives

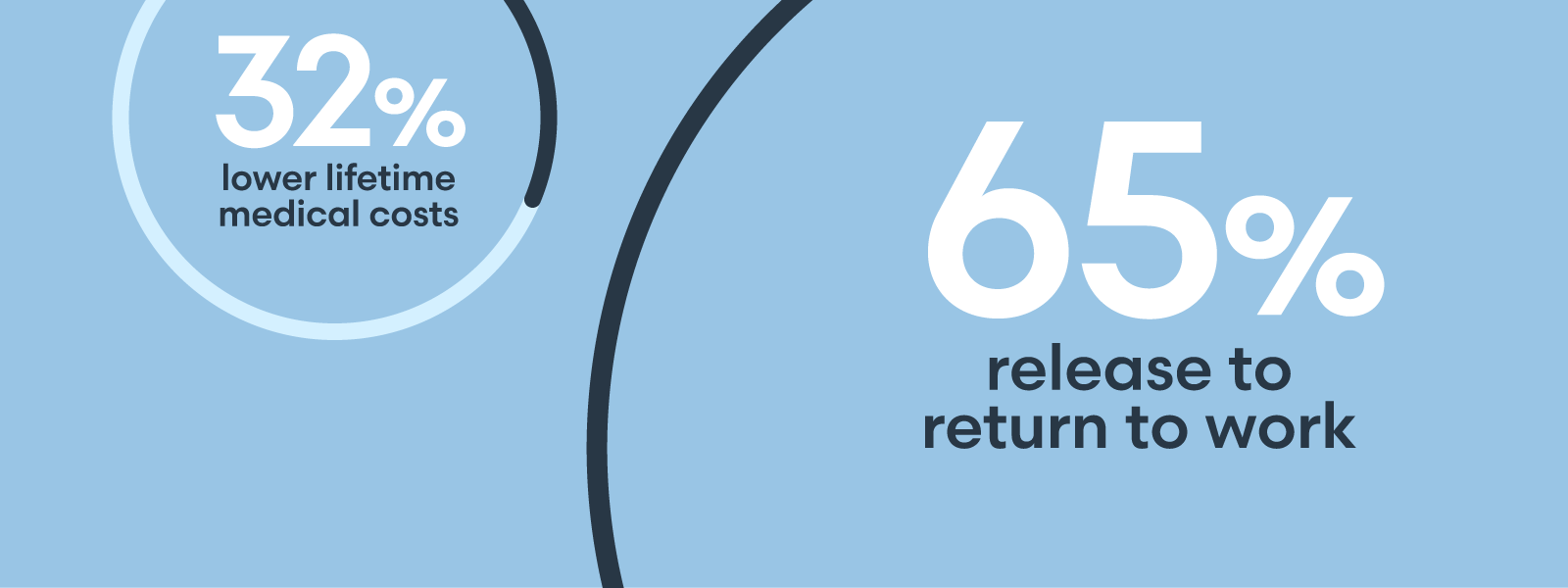

Self-funding pays off

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"