Five stop loss strategies to reduce risk

How self-funded employers can stay ahead of rising catastrophic healthcare costs

By Tara Krauss | President, Accident & Health, QBE North America The frequency of million-dollar claims has doubled over the past four years, and average large claims — particularly for neoplasms — now exceed $350K at the $200K deductible level. Chronic conditions like cancer and circulatory disease continue to drive these catastrophic claims, with circulatory diagnoses increasing in frequency by nearly 60% since 2020. According to QBE’s 2025 Accident & Health Market Report, these converging trends and more fuel uncertainty and cost escalation in today’s employer-sponsored healthcare plans. In response to mounting financial pressure, employers are increasingly relying on medical stop loss coverage. Approximately 63% of covered workers are enrolled in self-funded plans, and most of these organizations — particularly small to midsize employers — purchase stop loss insurance to protect against catastrophic exposure. But claims aren’t just rising in cost and frequency; they’re becoming more complex and unpredictable. For self-funded employers, this means that traditional assumptions about stop loss coverage — including deductible levels, contract structure or cost management strategies — need to be reevaluated. The role of stop loss coverage is evolving to help employers and benefits teams balance cost control with offering high-quality, competitive healthcare. To stay ahead of rising costs and complex risks, employers and brokers must treat stop loss as a dynamic part of their overall healthcare strategy. These five strategies can strengthen stop loss planning and reduce exposure to large, unpredictable claims. Employers often set a specific deductible and leave it untouched for years. But as healthcare costs rise, flat deductibles place more risk on the stop loss carrier, increasing the likelihood of renewal hikes or stricter contract terms. Consider a 100-life employer group with a $50K specific deductible. Based on historical data, they can expect around five stop loss hits per year. Without periodically adjusting that threshold, claim frequency and severity build, putting pressure on both the plan and the carrier. To stay ahead of the trend, employers should work closely with brokers and consultants to align deductibles with group size and risk tolerance. Regular reviews help ensure the deductible layer keeps pace with inflation and evolving claims patterns. Often, the largest, most complex claims are tied not only to the condition itself but also to the care setting. Care decisions, such as where infusion therapy is administered, drastically affect cost variability. Reviewing 12 to 36 months of claims data can help identify where and why these high-cost scenarios are occurring. Patterns such as late-stage cancer diagnoses, high-risk pregnancies or repeat hospitalizations often signal opportunities for earlier intervention. Understanding these patterns enables employers to more accurately predict stop loss breaches and develop more effective coverage strategies. With strong data insights, targeted vendor partnerships can help facilitate earlier intervention, reduce claim severity and improve outcomes. For example, oncology care management vendors can identify cancer diagnoses early and guide members to high-quality, lower-cost Centers of Excellence. Maternity programs focused on high-risk pregnancies can provide proactive support to reduce NICU admissions. By reducing the frequency and severity of large claims, vendor partnership strategies play a direct role in minimizing stop loss utilization and long-term premium volatility. 4 . Demand transparency from pharmacy benefit managers (PBMs) Pharmacy spend remains one of the most significant and challenging costs to manage in self-funded health plans, largely due to a lack of visibility into how pharmacy dollars are allocated. Rebate arrangements, drug pricing tiers and formulary decisions are often opaque, leaving plan sponsors without a clear sense of value or savings. Ask detailed questions: Where are the rebates going? How is the formulary structured? What evidence shows the PBM is truly lowering our pharmacy costs? Employers can also work with brokers to evaluate point solutions that address key cost areas, such as pharmacy navigation tools that guide members toward lower-cost alternatives, copay assistance programs and specialty drug case managers that can help reduce claims severity and improve outcomes. Chasing the lowest stop loss premium may seem fiscally responsible, but frequently switching carriers can introduce serious volatility. A single high-cost claim under a bargain-rate policy can trigger significant rate hikes or limited renewal options the following year. Choosing a financially strong, A-rated carrier with experience in healthcare underwriting can provide more long-term value. Employers should prioritize carriers that offer consistent contract terms, responsive claims support and the flexibility to evolve coverage as the plan matures. While renewal planning typically occurs between July and October, the most effective strategies take place year-round. Regularly reviewing claims history, identifying key cost drivers and aligning stop loss design to current population trends ensures that coverage stays in line with actual exposure and supports long-term plan sustainability. Working closely with brokers, consultants and vendor partners early in the cycle gives employers more options, more negotiating power and fewer surprises. QBE Accident & Health provides coverage and services to support the specialized needs of self-insured employers. To learn more, visit qbe.com/us and read the full 2025 Accident & Health Market Report here. Tara Krauss, President, Accident & Health, QBE North America QBE makes no warranty, representation, or guarantee regarding the information herein or the suitability of these suggestions or information for any particular purpose. QBE hereby disclaims any and all liability concerning the information contained herein and the suggestions herein made. Moreover, it cannot be assumed that every acceptable risk transfer procedure is contained herein or that unusual or abnormal circumstances may not warrant or require further or additional risk transfer policies and/or procedures. The use of any of the information or suggestions described herein does not amend, modify, or supplement any insurance policy. Consult the actual policy or your agent for details about your coverage. QBE and the links logo are registered service marks of QBE Insurance Group Limited. © 2025 QBE Holdings, Inc.5 stop loss strategies to help employers manage catastrophic healthcare costs

1. Right-size the specific deductible — and review it regularly

2. Identify what’s driving high-cost claims

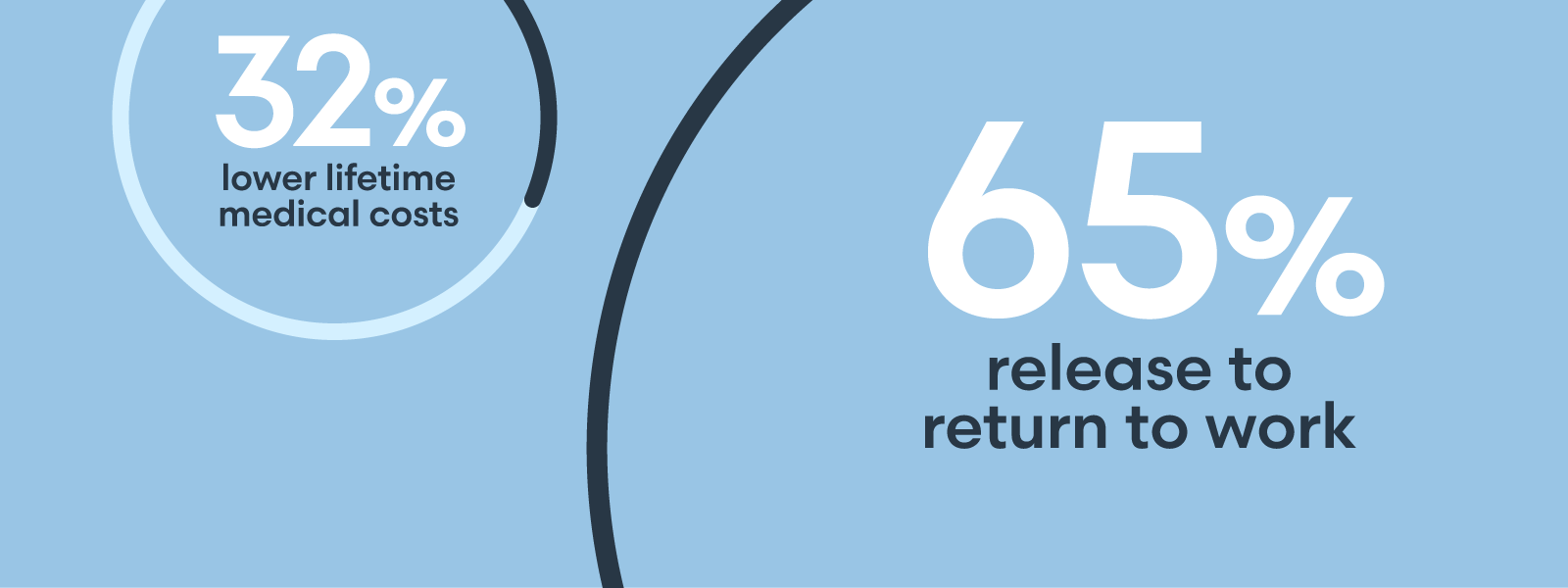

3. Leverage vendors to proactively manage risk

5. Choose a carrier based on consistency, not just cost

Plan ahead, not just at renewal

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"