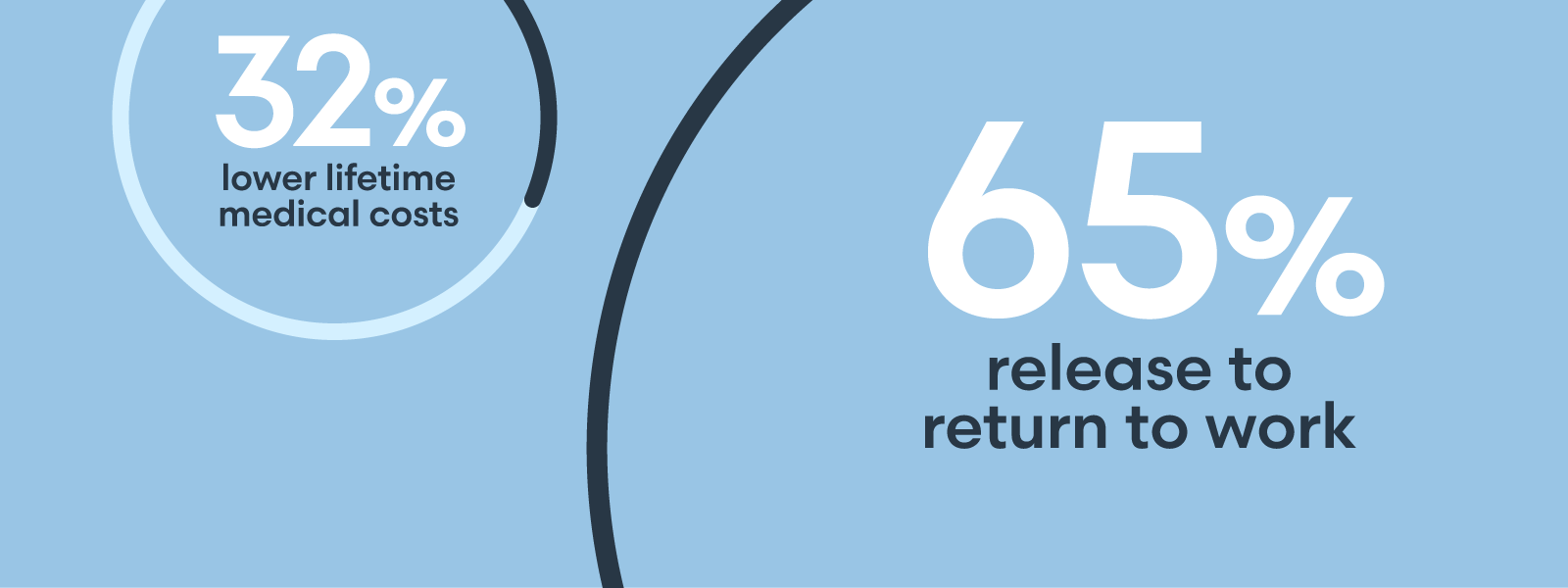

As risks become more interconnected, the need to break down data silos and increase data exchange with risk management partners is becoming a business imperative. Origami Risk’s Chris Bennett and Earne Bentley share their insights on why insurers, brokers, and risk professionals need to bridge and integrate their systems for understanding, analyzing, and keeping track of risk management and insurance information, to improve their collaboration and decision making involving interconnected risks. Bentley: On the insured side, there is definitely a “This is the way we’ve always done it” aspect to it. Manual procedures were developed around paper-based processes, and those same procedures were replicated in digital solutions without ever being changed much. Those traditions have created a fairly limited vision for what this exchange could provide and what problems the status quo approach is generating today. Bennett: The carrier side faces even greater headwinds, because carriers are siloed and complex organizations, which don’t tend to roll data up into a single system. In addition, the data itself is challenging because it changes over the course of a claim’s lifecycle. Shifting data would present a challenge to even the most data-savvy organizations. Before the pandemic, the insurance industry was a distant laggard in terms of digitization. So, it was already a little backward-looking with technology adoption. During the pandemic, however, many carriers made rapid advancements to enable remote work, which prompted them to evaluate the capabilities of their current technology and consider where they needed it to go. This proved the industry can make dramatic advancements when forced to do so. And now the pressures from a highly dynamic risk environment, paired with the compounding effects of inflation and supply chain shortages pressuring replacement costs, are leading carriers to start looking at the next potential way to weaponize technology to tackle that challenge. Enhancing the insured/insurer data exchange is an ideal way to do that. Bentley: It is absolutely both. Yes, you do need solutions that support seamless connections and data flows, which this approach demands. Legacy systems and “homegrown” solutions may not meet that bar, and manual processes are going to be particularly difficult to work around. Beyond the technical ability to capitalize on a better exchange, the essential question is, “Is your organization ready and willing to take advantage of all that new information?” Being “data driven” is sort of a cliche these days, but in this case it actually applies. To fully leverage the promise of this exchange, you need a culture that values data-driven decision making and is willing to explore new ways of doing business powered by the insight gained from that data. Without both components, you’ll never see the full benefits of this approach. Bennett: Silos form because they are necessary early in an organization's development. Each unit has their own goals and objectives that they are accountable for, so they find the best tools and processes to help them reach those goals. That turns into a problem when the tools and data that one department uses can’t “talk” to the tools and data in another department. Things get locked into silos, and the ability to connect the dots, see the bigger picture, and understand how what’s happening in one area affects another all gets lost. A siloed approach may initially have short-term benefits for a particular business unit, but in the long term the enterprise suffers and opportunities are left undiscovered. Silos built around commercial and personal lines are beginning to break down as policies cross those boundaries to meet evolving risk needs. For example, in the gig economy, drivers who use their vehicles for ride sharing may need a single policy that covers personal use as well as the business aspect, or mixed-used policies for home sharing. To ensure future growth in a relatively commoditized market, organizations will need to share data and think about enterprise-wide solutions. Bentley: While technology can definitely help overcome this challenge, it has to be the right type of technology. Solutions need to be designed with the intention of sharing data. Unfortunately, many risk technology providers have built out their solutions through acquiring other software providers and then bolting on the new functionality so it looks like it is “all under one roof.” The reality is that these systems weren’t designed to “talk to each other.” They function in completely different ways, and essentially just bring silos into the digital era. From the beginning, Origami Risk has taken a different approach. By building new components ourselves on a single platform, all the components understand each other, data can flow seamlessly between what used to be silos, and the door is open to leverage insights gained from a more unified view of the data. How can speed and automation of data exchange enhance risk management and risk transfer? Bennett: One thing abundantly clear in today’s risk environment is that time is not an ally. Both sides pay a cost when there are delays in the exchange. Lags result in outdated values, increased inflationary replacement costs, the risk of reserve inadequacy for carriers, and the missed opportunity to address issues earlier, at a lower cost. But if we move the exchange from an annual event to something more continuous that provides real-time data, we create more opportunities to strategize and take action based on up-to-date information. Insureds can understand the factors driving shifts in underwriting, and carriers can benefit from progress updates on mitigation efforts to more accurately price policies. Many carriers still receive weekly or monthly reports from third-party administrators, often in PDF or spreadsheet formats, that are just too late to act on. Underwriting actuaries need data that is close to real time, so they can revise their assumptions, manage hedges and answer pointed questions from their senior management. This kind of near real-time data exchange is the foundation of integrated risk management. The insured/insurer information exchange asks, “How can these two sides share information so that each benefits?” IRM is more about how we take the data each group has, connect it, and use that to see a fuller context that drives better decisions. Bentley: It’s about making sure data reaches all of those who can benefit from it. Changes in policy data — such as rate increases, higher limits, additional restrictions, etc. — are signs that underwriters have assessed the client is facing higher risks. From an enterprise risk management practitioners’ perspective, those data points are essentially key risk indicators that could help them complete their own risk assessments. Yet that type of data rarely is available to ERM professionals, so it never gets factored in. Conversely, other departments have data that could influence underwriting and total cost of risk. If, for example, an organization had a rise in a particular type of workplace accident and, as a result, the safety team implemented new procedures, tracked a decline in incidents, and verified progress with audits and other measurements, all that data should influence the next policy cycle. Yet the data may be spread out across multiple departments, each using different systems, with no easy way to consolidate the data. IRM provides a centralized platform on which each group can contribute and pull relevant data, making it easy to provide the insurer with a more accurate picture of risk and adjust pricing accordingly. Bentley: IRM allows for seeing a bigger picture that leads to better decisions. For example, safety data may trigger an alert notifying an enterprise risk manager of a spike in a particular workplace safety event. Claims data may then validate the rise in that risk. Elevating that risk in the risk register could trigger new safety programs and audits to see if the policies are being enforced. Compliance may benefit from audit data, while HR may need access to training data. And all that data then needs to get back to the risk manager to lower TCOR. That process is impossible if each group uses a system not designed to communicate with the others. Bennett: Carriers are affected by IRM approaches in two ways. The first is the internal use of IRM approaches. Given the highly complex, siloed, and regulated environment in which they operate, risk management is often done at the executive level through slide decks and spreadsheets. Without any practical way to roll up data and conduct trend analysis, there can be significant gaps in their understanding of the true cost of risk. A single-platform IRM approach reduces the burden for the executive, compliance, IT, and legal teams in developing a truly comprehensive view otherwise locked in separate systems. The second effect relates to client adoption of an IRM approach. It is in the best interest of every insurer and broker to have their clients leveraging single-platform IRM solutions. Underwriters benefit from having a better understanding of what mitigation efforts are in place, what the data shows in terms of progress, and how all of that translates into a lower risk evaluation. Beyond gaining a clearer understanding of the risk context for a client, carriers and brokers connected to their clients using an IRM platform can aid in risk mitigation efforts in more proactive ways than ever before. For example, carriers can use their access to data related to broader changes in the marketplace to help clients benchmark their progress, more easily identify early warning signs, and follow through with actionable items like engineering recommendations. This turns the carrier into a risk management partner that provides much more value than risk transfer alone. Bentley: The value proposition for brokers having their clients use an IRM solution is similar. To deliver the best guidance, they need the fullest picture of each client’s situation. IRM platforms help capture that information and produce reports that save brokers from having to assemble all of that data manually. This means more time spent providing insight to clients and less time chasing data. For more information about Origami Risk and IRM, download our 2023 State of Risk Report. Chris Bennett is President of Core Solutions and Earne Bentley is President of Risk Solutions at Origami Risk, a leading provider of integrated SaaS solutions for the risk and insurance industry. Highly configurable and completely scalable, Origami Risk delivers a full suite of risk management and insurance core system solutions from a single secure, cloud-based platform accessible via web browser and mobile app.Chris Bennett | President, Core Solutions, Origami Risk

Earne Bentley | President, Risk Solutions, Origami Risk

What’s stopping organizations from exchanging data more effectively with insurance partners?

Is it an organizational culture problem, a digital infrastructure problem, or both?

How do data silos form? What can organizations do to break those down?

What does IRM look like from the perspective of the policyholder?

What does IRM look like from the enterprise view?

How does IRM help underwriters and risk advisors?

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"