How to build the best excess casualty submission

As limits tighten and volatility rises, submissions and underwriter relationships make a significant difference

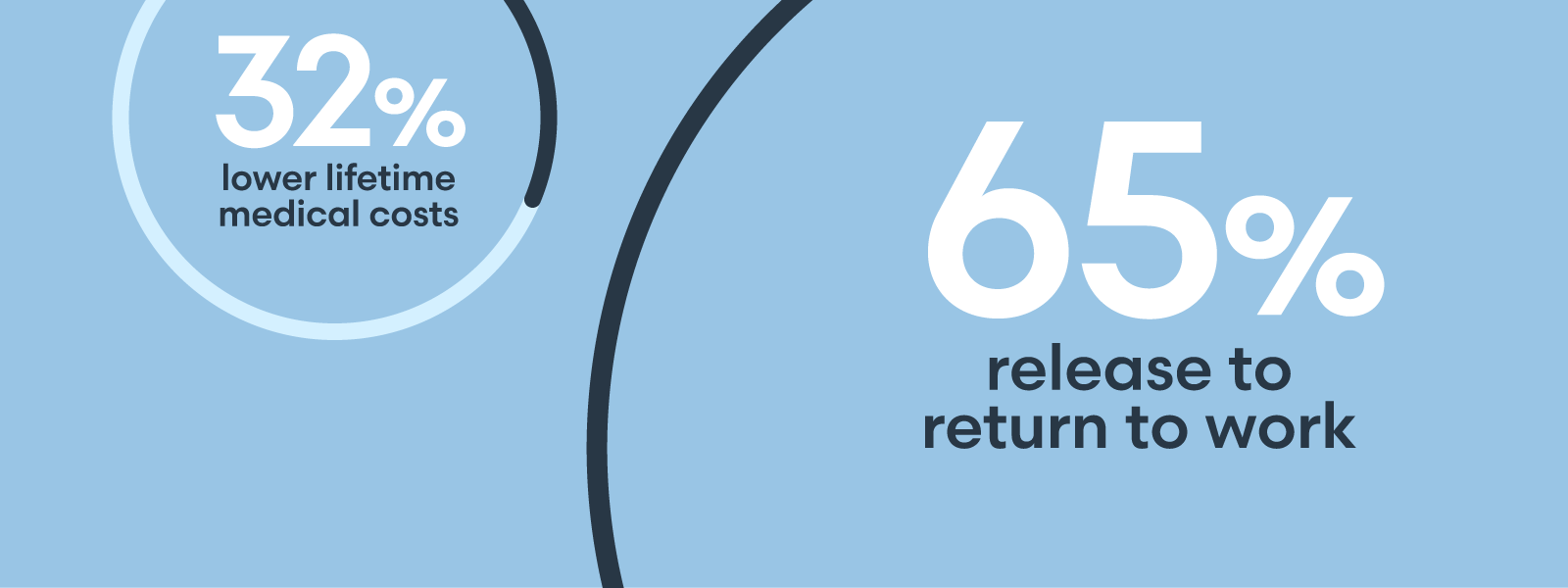

The excess casualty market in 2025 continues to expand rapidly, driven by higher policy rates and increased loss severity. Umbrella liability premiums grew 11% in Q2 2025, the steepest increase among major commercial lines, underscoring the ongoing strain on liability programs. Yet growing premium volume does not translate to abundant capacity. Carriers are offering shorter limits and deploying capital more cautiously, forcing brokers to assemble towers with more participants and handle last-minute shifts. Social inflation is compounding the strain. The mean nuclear verdict now reaches $89 million, raising stakes for brokers and underwriters alike. In this environment, success can depend not on chasing more capacity, but on how brokers and underwriters collaborate — enhancing engagement, presenting risks compellingly and navigating challenges side by side with strategic insight. Strong submissions go beyond spreadsheets and help underwriters build the case for offering the best possible quote. Highlighting self-insured retentions, safety programs and meaningful risk mitigation investments demonstrate to underwriters the insured’s commitment to managing risk. If a large loss has occurred, explain what was learned and what corrective actions have been taken. Insureds that can show they are proactive, reputation-conscious and focused on avoiding losses present a more compelling story. It also helps to showcase the strength of the tower itself. Underwriters writing high excess layers are assessing not just the insured, but the carriers beneath them. Demonstrating that highly-rated trusted markets are already in place at lower layers reinforces the stability of the overall program and supports stronger outcomes at the top. With capacity shifting at the last minute, incomplete or late submissions can derail a placement. Brokers should aim to provide at least 10 years of loss runs, a thorough outline of all exposures and the controls in place to manage them, plus renewal details as early as 90 to 120 days out from the renewal date. Well-prepared submissions not only help underwriters prioritize what matters most but also demonstrate the broker’s commitment to transparency and partnership. Early communication by both brokers and underwriters reduces the risk of unpleasant surprises if limits or terms change close to renewal and creates more room for collaborative solutions. As limits contract, some insureds may be tempted to buy less coverage. An alternative approach is to maintain tower protection while exploring captives or structured programs to manage costs and fill lower layers. Offering alternatives signals that the insured is committed to managing risk strategically rather than simply reducing spend. It also positions brokers and underwriters to work together with greater confidence, knowing the client is engaged and actively participating in the risk management process. Each carrier has its own sensitivities — whether PFAS liability, abuse and molestation claims or other exposures. Submissions that acknowledge and address these concerns make it easier for underwriters to respond quickly and confidently. Understanding which markets prioritize rate above other metrics gives brokers the insight to shape placements more effectively. For example, whether an underwriter will trade a higher attachment point for a shorter limit lower in the tower, or whether a carrier has mandatory exclusions that must be attached. By anticipating these priorities and constraints, brokers and underwriters can work together to build programs that balance capacity and coverage in ways that serve the insured best. In excess casualty, opportunities often emerge at the eleventh hour. Underwriters may be able to slot into a tower as late as the day before binding. Brokers who stay engaged through closing — and keep underwriters informed of potential moves — are less likely to be left with gaps. Underwriters who remain available and able to respond to last-minute opportunities can often solve critical problems for brokers with gaps to fill. Management plays a key role in facilitating these opportunities by equipping underwriters with the tools, training and authority they need to act swiftly and confidently in time-sensitive scenarios. This responsiveness not only helps close placements, but it also reinforces to brokers that they can rely on their markets for support when it matters most. Notwithstanding, last-minute engagement should not mean abandoning discipline. The best outcomes often emerge when brokers communicate changes quickly and underwriters maintain guidelines while still providing solutions. Relationships remain the linchpin of successful placements. When brokers and underwriters communicate consistently, understand an underwriter’s priorities and exchange the right information at the right time, both sides are better positioned when towers shift unexpectedly. These relationships also enable candid conversations about what matters most — whether rate, limit or coverage terms — and help secure creative solutions when pressure is highest. The excess casualty market in 2025 is defined by growth, but also by fragmentation and strain. Higher premium volume masks the reality of shrinking limits, last minute shifts and escalating loss severity. For brokers and underwriters alike, success may be found in any market cycle when execution on both sides is strong. By partnering together — encouraging earlier preparation, maintaining continuous communication throughout the submission process and focusing on the quality of both clients and the towers supporting them — we can build programs that inspire confidence. These joint efforts position us not only to navigate today’s volatility, but to turn it into competitive advantage and future opportunity. By Mary Horsch |Senior Vice President, Head of Retail Excess Casualty at NationwideTell the insured’s story.

Provide complete and early submissions.

Explore alternative structures.

Know your markets and their hot buttons.

Stay engaged until binding.

Invest in the underwriter relationship.

Turning volatility into opportunity

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"