Bankruptcy risk rising amid economic uncertainty

How management and professional liability insurance protects businesses and leaders when financial pressure turns into legal exposure

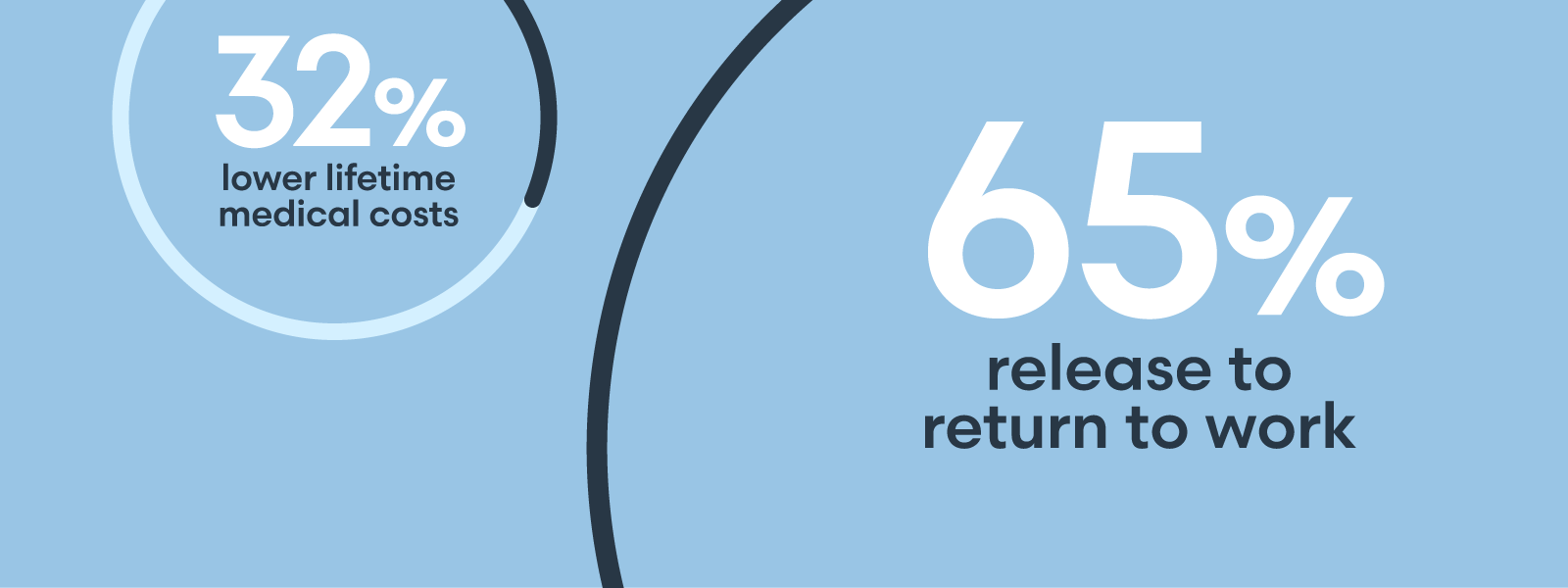

Over 370 corporate bankruptcy filings occurred in the first half of 2025 — the highest for any six-month period since 2010. This reflects a broader economic strain. Persistent inflation, high interest rates, regulatory scrutiny, and softening consumer demand are placing added pressure on businesses, particularly private and mid-sized firms. This resurgence in bankruptcy activity signals a growing wave of management and professional liability risk. Financial stress often triggers legal action against company leadership, including investor lawsuits, employment-related disputes or internal misconduct. Unlike larger organizations, private firms often lack the internal controls or liquidity buffers to weather these storms, making insurance coverage critically essential to avoiding a mistake from which they can’t recover. When financial pressure mounts, management teams are forced to make difficult, high-stakes decisions. Layoffs, reorganizations, cost-cutting, and subsequent investor communications all carry legal implications. In these moments, management and professional liability insurance serves not only as protection but also as a stabilizing force, allowing leaders to act decisively without fearing personal or organizational ruin. A well-structured program can: Enable confident leadership in a crisis by ensuring directors and officers have personal protection in the event of legal action Support a timely legal response with access to counsel and defense resources should allegations arise Preserve continuity by covering the costs of claims that might otherwise drain operating cash or interfere with restructuring efforts Strengthen board and investor trust, reassuring stakeholders that risk has been planned for, even in worst-case scenarios Each layer of coverage — from directors & officers (D&O) to employment practices liability (EPL) — acts as a financial backstop against a different category of risk. When claims happen in quick succession during a downturn, these protections help ensure the business can survive the storm and that its leaders are shielded from personal liability. The following are four key coverage areas for businesses to focus on: D&O insurance protects directors and officers against claims of mismanagement, breach of fiduciary duty, or misleading investors. In bankruptcy, this coverage is often the only asset left to resolve litigation. Companies should review policy limits to confirm they have A-side coverage for individual executives and examine potential gaps — especially in areas like insured vs. insured exclusions. EPL insurance is especially critical when layoffs or restructuring lead to wrongful termination or discrimination claims. In high-stress environments, employment-related disputes tend to increase. EPL helps cover legal defense and settlement costs at a time when resources are already stretched. Fiduciary liability coverage responds when employees or retirees allege mismanagement of retirement or health plans. Cutting or suspending benefits during a financial downturn — without proper documentation or communication — can expose companies to ERISA-related claims. Ensuring appropriate fiduciary limits now can avoid compounding legal exposure later. Crime insurance helps protect against internal fraud, embezzlement, or theft. Financial hardship, layoffs, and weakened oversight all increase the risk of insider misconduct. Claims of this nature surged during COVID and may be expected to rise again in periods of economic strain. Risk transfer alone isn’t enough. While strong management and professional liability coverage can protect a business and its leaders during a crisis, the goal is to avoid reaching that point altogether. Proactive risk management doesn’t just reduce the severity of claims — it also helps businesses remain solvent, compliant, and resilient as conditions shift. Key risk management practices include: Scenario planning: Develop contingency strategies in case revenue declines, loans aren’t renewed, or refinancing fails. Create “Plan B” frameworks that outline how the business would respond to layoffs, margin compression, or restructuring — before those actions become urgent. Strengthening compliance infrastructure: Regulatory scrutiny is growing, particularly around tariff enforcement and pandemic-related funding. Proactively review documentation and internal controls to ensure they’re audit-ready. Clear stakeholder communication: Keeping investors, boards, lenders, and employees informed builds trust and reduces the likelihood of litigation from those who feel misled or excluded during difficult decisions. Consult with legal counsel on these communications. Working with brokers and advisors early: A broker can help identify gaps in coverage, propose additional layers or limits, and tailor insurance programs to align with the current risk profile. As bankruptcy and litigation risk rise, management and professional liability programs become essential to preserving business continuity and personal protection for leadership. For private companies in particular, now is the time to reassess coverage, close gaps, and prepare for what comes next. Because in bankruptcy, the policy is often the last line of defense, and how well it’s structured may determine what survives the fallout. By Nan Murphy | Senior Vice President, Management Liability, Munich Re Specialty – North America Munich Re Specialty is a leading provider of management liability coverage for private companies and not-for-profit entities. Its underwriters, claims teams, and risk consultants help businesses navigate complex financial and legal exposures with confidence. Learn more about Munich Re Specialty – North America’s Management Liability solutions: https://www.munichre.com/specialty/north-america/en/solutions/management-liability.htmlManagement and professional liability policies deliver value during economic downturns

Proactive risk management for uncertain times

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"