Commercial auto insurers have had a combined ratio over 100 for the past 11 years, indicating that, on average, the industry is not profitable—at least not turning an underwriting profit. That said, there are insurers in this line of business that are successful. Two of the bigger reasons behind profitability challenges have to do with external trends. Number one: Inflation hit a 40-year high this year, which together with supply chain issues is driving up claim severity and loss costs. While this is a more recent phenomenon, "social inflation," also known as nuclear verdicts in lawsuits involving commercial drivers, has increased even faster than the rate of inflation. Triple-I estimates commercial auto is the line of business most impacted by social inflation, and according to their study, it has led to $20 billion in additional commercial auto liability claims over the decade leading up to 2020. A second factor identified by analysis we've conducted at Verisk suggests an emerging pattern of riskier driving behavior. We first witnessed this during the pandemic lockdowns of 2020 on roads that were initially nearly devoid of traffic. More severe accidents and sever violations didn't decline as quickly as overall accidents and minor violations, and this pattern shows signs of carrying forward. There are other external factors, such as the growth in aggregate mileage across the commercial sector, the increase in last-mile deliveries, and the related driver shortage which can influence the hiring of less experienced and riskier drivers. There are many similarities between the lines, and if you want profitable growth, it's critical for insurers to evaluate and price risk accurately. Both lines need to assess risk for drivers and vehicles. Credit-based insurance scores help measure the financial risk of individual drivers and business owners, and factors such as garaging address can have significant differences in associated rating relativities. Similarly, vehicle registration reports can help correct a book of business by validating vehicle registration information and identifying potential sources of premium leakage related to a specific vehicle such as branded titles. At Verisk, we believe data and analytic accuracy are critical to assign the right price to the right risk. And we strive to bring the latest quality data sources combined with our 50+ years of actuarial expertise to bring powerful analytics and innovation to the industry. I mentioned industry challenges such as mileage shifts: A Verisk study shows that commercial auto insurers will lose more than $1.5 billion this year to premium leakage over mileage radius misclassification alone. Innovations like our RadiusCheckTM solution, which uses cutting-edge technology to take photos of license plates and match them to vehicles in an insurer's portfolio, can help close the gap in getting to profitability since radius misclassification can have large premium impacts. Each sighting is tagged with a latitude and longitude and a date and time stamp to help identify when and how often an insured vehicle is traveling outside of its radius. While commercial auto underwriting leaders must evaluate many of the same risks that personal auto insurers assess, in many ways their work overlaps with that needed to write small commercial or business owners' policies. Reliable business information matters. Our internal analysis demonstrates that 50 percent of businesses fail in the first five years, and further, 50 percent of the high-level industry codes are inaccurate in the typical carriers' book. To price accurately, insurers need to know how to properly classify a business they are insuring and understand how they are using the insured vehicles. Verisk's Auto Firmographics is an innovative solution that commercial auto insurers can leverage to address this challenge. Speed and accuracy are important in commercial auto just as in personal auto or BOP, and solutions such as Vehicle Prefill help insurers to reduce time to quote and improve quoting accuracy by pulling in all vehicles registered to a business in one easy API call. I mentioned the driver shortage and riskier driving behavior earlier. To ease supply chain issues, federal legislation was passed recently, giving the green light to 18-20-year-old, cross-state, big-rig drivers in a test apprenticeship program. Drivers this young were previously not allowed to handle this type of driving, and there are a lot of questions about the safety of this program as well as requirements to restrict access based on driving behavior. Verisk now has a new solution built on more than 1.7 billion court records of driving violations, as well as 50 million police and accident reports. We encourage commercial auto insurers to put us to the test to see how these new data sources can help provide lift and cost-effectively assist with assessing driver risk. We're also seeking development partnerships if an insurer wants to be in the driver's seat, so to speak, on emerging use cases for these innovative data sets. Lastly, just as personal auto insurers have transformed digitally and added usage-based insurance options to meet the needs of the modern insurance buyer, I see an InsurTech revolution ahead for commercial auto. Verisk will be right there to help with solutions such as straight-through processing and telematics, transforming the commercial auto landscape for what comes next.

The profitability challenges of commercial auto insurers are well documented. Why is this occurring?

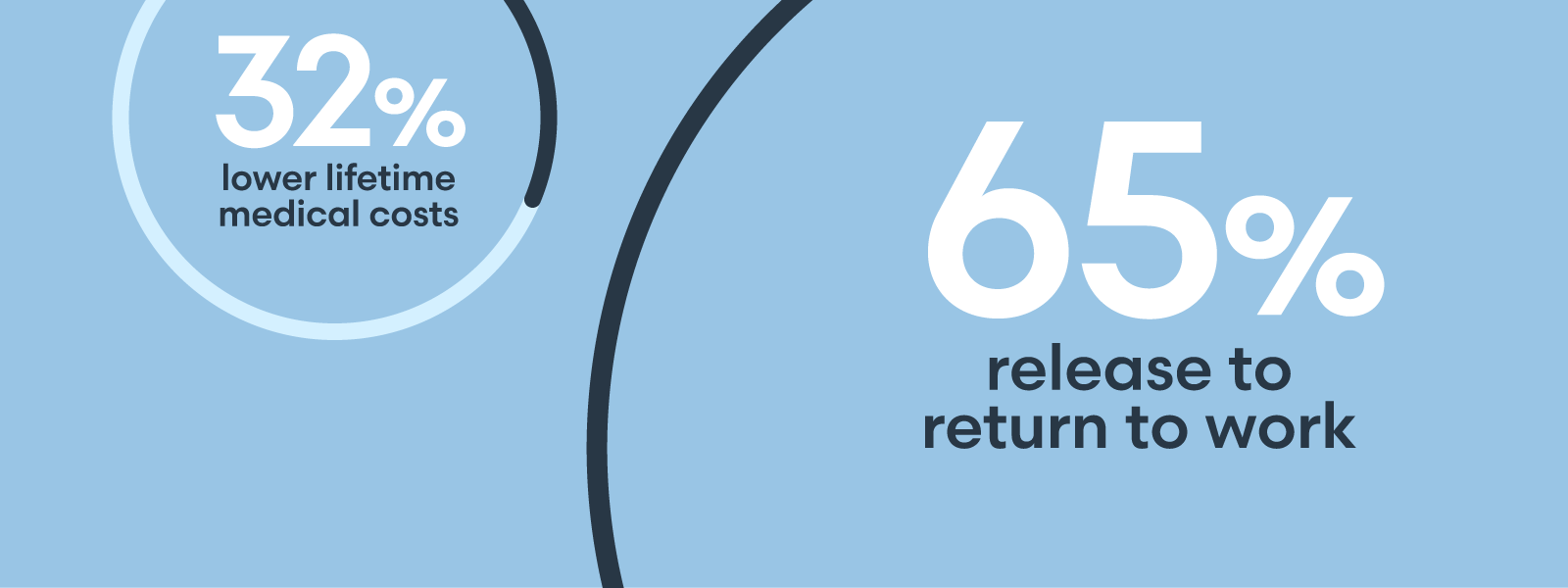

Personal auto insurers have generally been more profitable than their commercial auto counterparts. Are there similarities between the lines and perhaps lessons that can be applied in a commercial context?

Are there similarities between commercial auto insurers and other lines of business?

Are there other innovations Verisk is working on? What do you see impacting the industry next?

Greg Jacobs is a Director in the Auto Product Risk Assessment Group at Verisk. He leads the teams managing several products including the Commercial Auto and Telematics offerings.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"