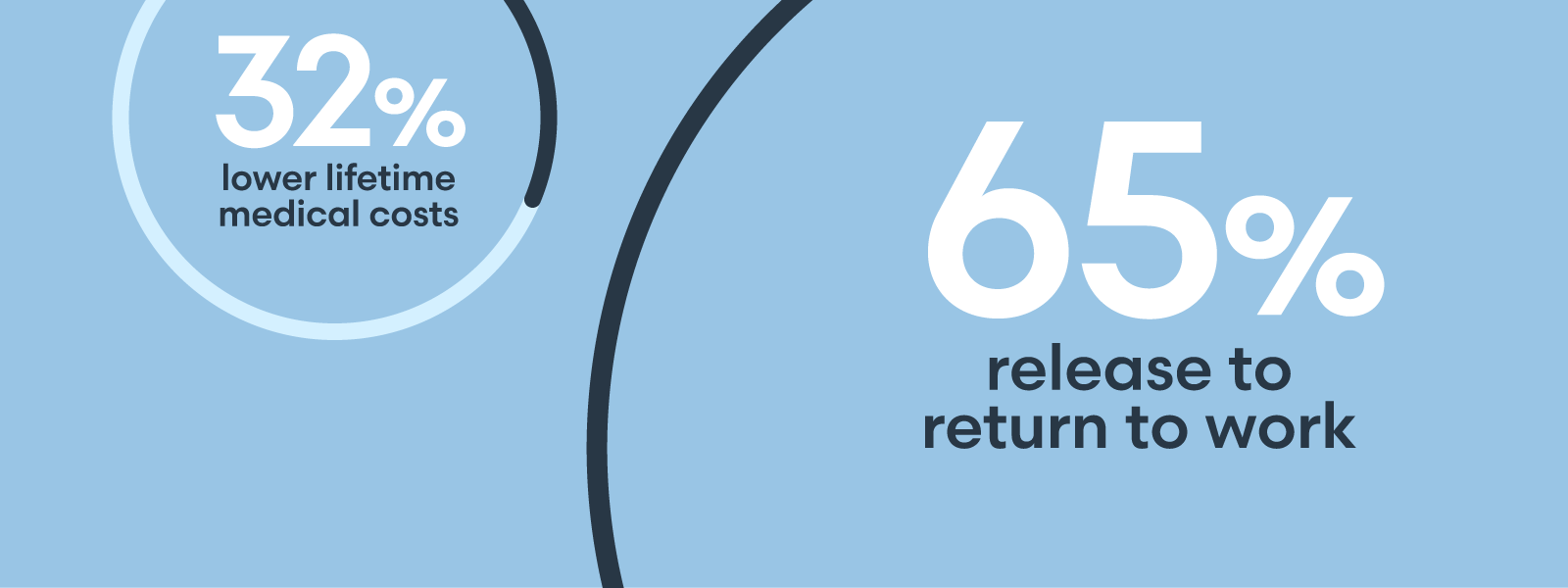

Underwriting property risk in years past used to be a relatively straightforward proposition. After determining whether a given property had a catastrophe exposure, underwriters’ next question was likely to be, “Is it a good fire risk?” Today, however, property owners and their insurers have a lot more to take into consideration, as loss drivers are shifting. Water damage is very real and has become key driver of loss in commercial property insurance. Other types of losses, such as convective storms and wildfires, also can pose big problems depending on the nature of construction, property location and loss control measures in place. Economic inflation is changing property valuations, which can result in coverage gaps if policyholders haven’t examined their replacement costs recently. One of the major changes in property underwriting is the need for all parties – the policyholder, risk advisor and insurer – to have better data on the specific risks. While it’s not easy to predict what will be a costly loss that impacts a business, it is essential for property owners to take proactive measures to help protect their company and assets. Partnering with an experienced insurance company can be mutually beneficial to highlight mitigation efforts undertaken by a business owner. As a result, property insurers are asking agents, brokers and policyholders to provide more detailed information in coverage submissions. At The Hartford, our team values well thought-out submissions that accurately convey the risk characteristics and any loss prevention or risk management that could improve the risk profile. For example, the traditional elements known as COPE – type of construction, occupancy, protection, and exposure – are foundational to evaluating property risk. We also use interactive tools and third-party data sources to provide more insight on valuation and other characteristics. Having a wealth of data is a double-edged sword: more data points offer a higher-resolution picture of a given risk to underwriters, but they also provide more data to evaluate when making risk decisions. Getting valuation right is important for several reasons, not least is helping property owners avoid coverage gaps when they experience a claim and maintain access to adequate protection. Due to inflation and supply chain challenges, construction materials such as lumber and drywall are more expensive than they were 24 months ago, and an additional cost driver is skilled labor, which is in high demand but short supply. Added together, it costs more to repair or replace components following property damage. Risk managers can help reduce property risks and gain favorable consideration for their organizations’ assets with several steps. One is to carefully consider the exposures in their property schedule. These might include: Water. If damage from a flood or storm surge, similar to what occurred in downtown Manhattan during Superstorm Sandy, is a possibility, they should consider relocating mechanicals and other sensitive equipment to a higher floor or installing ballasts and barriers to resist water intrusion. At a minimum, Water Damage Prevention Plans should include having someone present who knows how to shut off water flows in the event of a leak. Wind. Installing a new roof to comply with building codes such as the Miami-Dade County, Florida, hurricane standards, or changing window glazing to increase their resistance to windborne debris, can go a long way toward reducing property damage. Upgrades and maintenance. Property owners should account for system upgrades and maintenance in their capital expenditure programs. It also can help to conduct periodic visual inspections of building components as well as infrared inspections of electrical systems. Report loss prevention investments. Sometimes property owners spend significantly on preventative measures but overlook including those in their insurance submissions. If the property underwriter knows about such investments, it may be possible to gain credit for those in the form of additional limits, relaxed terms/conditions, or lower rates. Utilize risk engineering resources. The Hartford gives most property policyholders access to our highly engaged and competent risk engineering team. The Hartford strives to assist customers, by pointing out opportunities to reduce risk for their business. We are committed to helping our policyholders improve their risk management, so they can grow their businesses. To learn more about our consultative and collaborative approach to property risk management, please visit thehartford.com. Andy Simmons is the Head of Business–Large Property for The Hartford Financial Services Group. The information provided in these materials is intended to be general and advisory in nature. It shall not be considered legal advice. The Hartford does not warrant that the implementation of any view or recommendation contained herein will: (i) result in the elimination of any unsafe conditions at your business locations or with respect to your business operations; or (ii) be an appropriate legal or business practice. The Hartford assumes no responsibility for the control or correction of hazards or legal compliance with respect to your business practices, and the views and recommendations contained herein shall not constitute our undertaking, on your behalf or for the benefit of others, to determine or warrant that your business premises, locations or operations are safe or healthful, or are in compliance with any law, rule or regulation. Readers seeking to resolve specific safety, legal or business issues or concerns related to the information provided in these materials should consult their safety consultant, attorney or business advisors. All information and representations contained herein are as of June 2023. The Hartford Financial Services Group, Inc., (NYSE: HIG) operates through its subsidiaries, including the underwriting company Hartford Fire insurance Company, under the brand name, The Hartford®, and is headquartered in Hartford, CT. For additional details, please read The Hartford’s legal notice at www.thehartford.com. By Andy Simmons | Head of Large Property, The Hartford

What insurers are seeking

Steps risk managers can take

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"