A market under pressure

5 trends currently defining the Casualty market

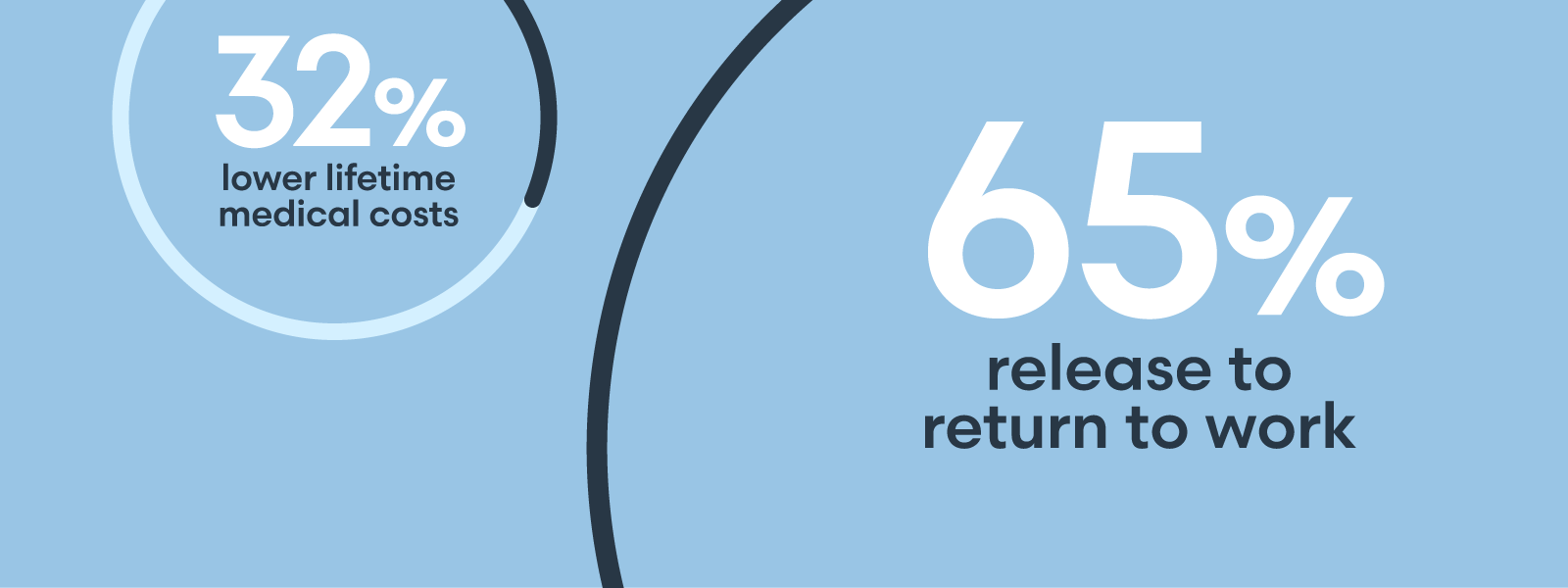

By Matt Hale |Head of U.S. Casualty Underwriting Operations Loss costs are surging, and casualty lines — once dependable anchors of the P&C insurance industry — are now among its biggest vulnerabilities. Nuclear verdicts, prolonged litigation, and a well-funded plaintiffs’ bar backed by third-party litigation financing have reshaped the risk landscape and challenged the limits of traditional underwriting. The numbers are staggering. Over the past decade, U.S. juries have delivered more than 1,200 nuclear verdicts — awards of $10 million or more — involving products, auto, general liability, and medical malpractice cases. Nearly 20% exceeded $50 million, and over 100 surpassed $100 million — called thermonuclear verdicts — in recent years, setting new records. Litigation financing has only added fuel to the fire, empowering plaintiffs to pursue aggressive claims strategies while turning down reasonable settlement offers in hopes of obtaining a nuclear verdict. At the same time, the legal system is digging out from its COVID-era backlog, and there is a cultural shift that can’t be ignored: 71% of Americans now believe large corporations have a negative impact on the country. Underwriters face immense uncertainty, not just in claims frequency, but in the severity and unpredictability of outcomes. Umbrella layers — once considered remote — are now being reached with regularity, as the traditional margin of safety has become a flashpoint. The result: more pressure on underwriting, more friction in dealmaking, and more fragmentation in how risk is shared. These headlines are just the starting points. What’s unfolding beneath the surface is a deeper shift in how insurance does business in a modern world. Here are five trends currently redefining the casualty market and what risk leaders need to be watching to come out on top: 1. Negative sentiment around insurance carriers Like that of large corporations and banks, public sentiment toward insurers — especially large, commercial carriers — has deteriorated in recent years. Whether it’s trust with their personal data — under 47% of global consumers trust businesses with their data— or with their best interests, insurers are faced with a culture of growing skepticism around every corner. The tragic 2024 shooting of United Healthcare CEO Brian Thompson brought longstanding public frustrations to the forefront with consumers voicing anger over denied claims and perceived prioritization of profits over “people.” This mistrust has real business consequences: greater scrutiny, more regulatory friction, and a jury pool more inclined to reach a verdict against insurers in court. It’s not just a reputational challenge: it drives up compliance costs, fuels legal exposure, and makes every denial, delay, or dispute feel like a test of public legitimacy. 2. Risks have grown bigger, broader, and are harder to assess Underwriters used to model coverage for $100 million construction projects, and now they’re facing $10 billion megaprojects with global footprints, layered ownership structures, and evolving liabilities. And these projects aren’t rare. Recent years have seen the start of 30-40 megaprojects per year (each valued at $1 billion or more), and U.S. companies that began in one sector, like tech, are now buying schools or hospitals. Private equity firms are entering sectors like healthcare. The result is a dizzying level of risk layering. One insured might be a great operator in one vertical and a complete wildcard in another. The lack of clarity makes it harder to assess exposure accurately and easier for underwriters to miss something consequential. 3. Additional layers of complexity for coverage towers In today’s volatile environment, building coverage towers has become a logistical chess match. Where four carriers might have built a $100 million tower with $25 million apiece, now 10-25 carriers may take $5 million slices (or even less) to diversify their exposure. That fragmentation creates not only coordination challenges but friction when claims hit, especially as more of them reach into umbrella layers. Carriers are increasingly quick to tender their limits and settle, often to avoid protracted litigation and the rising threat of bad faith accusations from others in the tower. While much of the recent focus has been on auto liability claims and the use of telematics — real-time driver behavior data — to mitigate losses and raise underlaying attachment points, umbrella carriers are just as often impacted by general liability (GL) claims. One large GL claim — a slip and fall, a concert stampede, a high-profile product failure — can wipe out years of premium. With savvy plaintiffs’ attorneys exploiting every avenue to trigger coverage, that risk is no longer hypothetical. 4. Every transaction takes longer The days of “quote and close” are long gone. Underwriters now spend more time explaining pricing, justifying positions, and navigating complex deal dynamics. Even when 20 carriers align on a structure, one outlier can throw the placement into flux. Deals are slower, stickier, and more vulnerable to derailment, leaving underwriters balancing actuarial discipline with pressure to close and retain key accounts. 5. The current environment isn’t reflective of actual losses in the industry Despite rate increases — casualty premiums have risen 8% annually over the past five years — the market still isn’t sustainable. Loss costs continue to outpace premium growth, and carriers still continue to post combined ratios over 100 and adjust reserves. Other lines like property and workers’ comp may be profitable, but they’re often propping up underperforming casualty portfolios. Meanwhile, competition from MGUs, global markets, and savvy brokers keeps pricing pressure high — making it hard for carriers to course correct without risking share. With volatility as the new normal, partnering with an experienced casualty carrier — one with a strong balance sheet that can think creatively about your complex risk — will give your business a leg up. BHSI prides itself on precisely this solution-oriented approach to casualty risks. We collaborate closely and transparently with our customers and brokers, building long-term relationships on a foundation of stellar financial strength. To learn more about BHSI, reach out here. Matt Hale is Head of U.S. Casualty Underwriting Operations at Berkshire Hathaway Specialty Insurance. Matt has been in the insurance industry for 23 years. Contact Matt in Chicago at 312.702.2802 or [email protected]. Berkshire Hathaway Specialty Insurance (www.bhspecialty.com) provides commercial property, casualty, healthcare professional liability, executive and professional lines, transactional liability, surety, marine, travel, programs, accident and health, medical stop loss, homeowners, and multinational insurance. The actual and final terms of coverage for all product lines may vary. It underwrites on the paper of Berkshire Hathaway's National Indemnity group of insurance companies, which hold financial strength ratings of A++ from AM Best and AA+ from Standard & Poor's. The information contained in this article is for general informational purposes only and does not constitute an offer to sell, or a solicitation of an offer to buy, any product or service. The advice of a professional insurance broker and counsel should always be obtained before purchasing any insurance product or any other service. The information contained in this article has been compiled from sources believed to be reliable. No warranty, guarantee, or representation, either expressed or implied, is made as to the correctness or sufficiency of any representation contained herein.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"