Parametric insurance: Addressing a multitude of risk scenarios

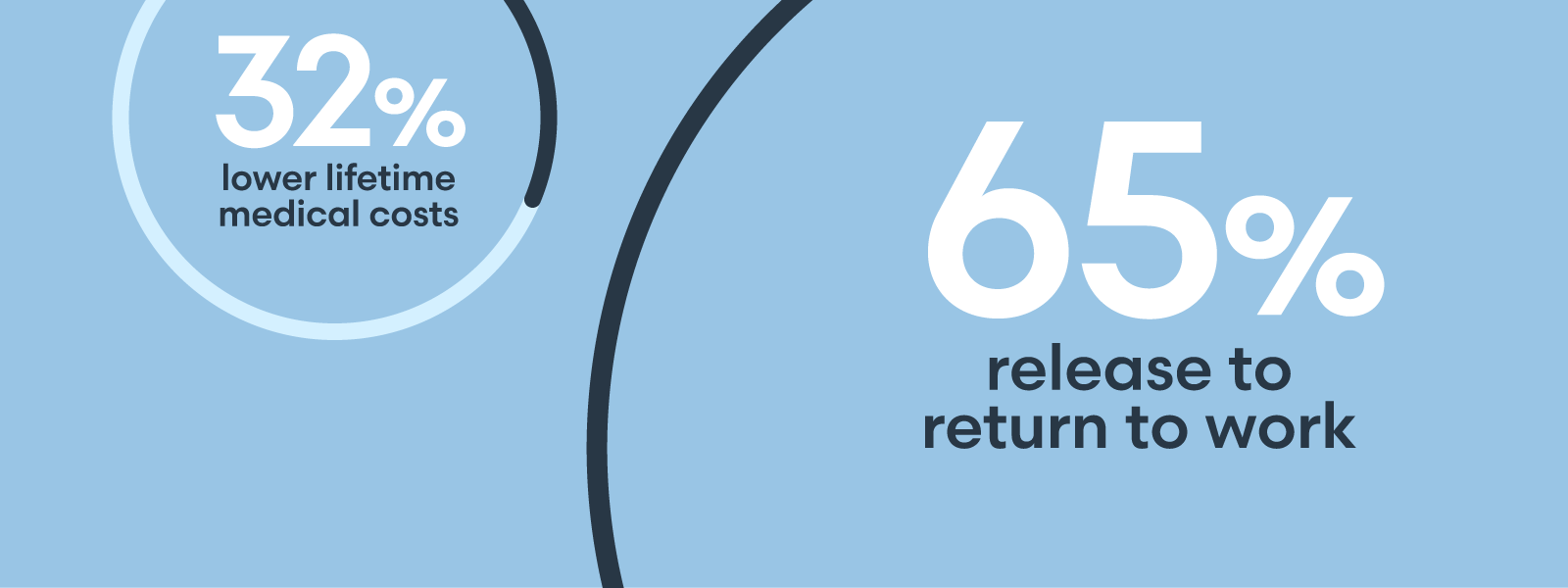

The risk environment is becoming more challenging, with an increase in extreme weather and natural catastrophe events, leading to a constrained market for traditional risk transfer solutions. Difficult as these conditions are for insurance buyers, they also open the door for creative risk-financing options. Parametric insurance is one innovative approach that is attracting wide interest. Insured losses resulting from natural disasters are up, causing disruption and financial stress for businesses of all sizes. So far in 2023, the National Oceanic and Atmospheric Administration (NOAA) has tracked a record 24 events that have caused at least $1 billion in economic damage across the United States. These natural disasters range from severe convective storms to flooding to hurricanes. A significant protection gap exists for natural catastrophes. In the United States between 2013 and 2022, the difference between economic and insured nat cat losses was $448 billion, or 43%, according to Swiss Re. Parametric solutions can help close that gap. Traditional lines of insurance, especially property, have responded to uncertainty by sharply increasing rates, reducing capacity and tightening terms and conditions. Some insurers also are imposing coverage restrictions on certain geographies and risk classes. Parametric solutions can provide financial protection in ways that traditional risk transfer methods cannot. As its name implies, parametric insurance is built around parameters that frame a given risk. In other words, if a scenario can be measured and indexed with robust historical, quality-controlled third-party data, a parametric contract likely can indemnify for it. Risks that are commonly transferred through parametric insurance are natural catastrophes in peak zones – such as California earthquake and Florida windstorm – and weather events such as extreme temperatures, excess rainfall or snow, hail, and tornadoes. Parametric solutions can apply, however, to a vast set of diverse risks. Parametric solutions are often used to supplement traditional coverage. They offer a way to transfer economic risk and close the protection gap. Parametric insurance also can address emerging or novel risks for which traditional insurance is unavailable or limited. Such risks include non-physical damage, cloud computing outages, and risks arising from a changing climate. As an example, severe convective storms (SCS) are a growing threat, responsible for 70% of global insured losses in the past few years. During the first half of 2023, SCS caused a record $38 billion in insured losses in the United States. Aon data shows that from 1990 to 2022, SCS losses increased at an annual rate of 8.9%. Parametric solutions are well-suited to address these kinds of losses. Additional advantages of parametric solutions include: No requirement for insurable interest. In traditional insurance, underwriters typically require policyholders to have an insurable interest in the asset. Parametric solutions allow clients to transfer economic risk associated with the failure of coverage for non-owned assets. For example, a business that relies on activities at a port it does not own could structure a parametric policy for business interruption losses triggered by disruption of the port operations. Most traditional property policies providing business interruption coverage require physical loss to an owned asset; the economic risk of a port shutdown would not be insurable under traditional policies. Rapid claims response. Parametric policyholders can have access to liquidity within days of an event that triggers coverage. Unlike traditional property/casualty insurance products, parametric policies do not involve conventional loss adjusting, which helps accelerate the claims process and improve transparency in settlement. Scalability. Significant capacity available on both a single carrier and syndicated basis. Performance measurability. With traditional risk transfer products, it’s difficult to determine how they might perform if a similar event were to occur today. Parametric solutions enable buyers to analyze historical or hypothetical modeled events and know with certainty how the coverage would respond. This can help insurance buyers make better-informed, more confident decisions about their risk transfer strategies. Parametric insurance can have a significant impact on an organization of any size's ability to recover following a major event. In many instances, the immediate access to capital is especially critical for organizations previously incorrectly thought of as being "too small" for a parametric solution. Any business in any industry with an exposure to extreme weather or natural catastrophes should consider how parametric policies can supplement existing traditional property coverage. For more information on Aon’s parametric solutions, please visit www.aon.com. Colin Harper and Peter E. Lacovara are Managing Directors of Alternative Risk Transfer & Innovation for Aon plc.By Colin Harper | Managing Director, Alternative Risk Transfer & Innovation, Aon

and Peter E. Lacovara | Managing Director, Alternative Risk Transfer & Innovation, Aon

Parametric insurance can be a valuable tool

Who should consider parametric solutions

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Lorem ipsum dolor sit amet, consectetur adipisicing, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut. Ut ad minim veniam.

Vestibulum ante ipsum primis in faucibus orci luctus etel ultrices posuere cubilia Curae.

Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut.

Sed ut perspiciatis unde omnis iste natus error sit voluptatem!

Nemo enim ipsam voluptatem quia voluptas sit odit aut fugit!

Ut enim ad minima veniam, quis nostrum exercitationem ullam!

"Et harum quidem rerum facilis est et expedita distinctio!"

"Nam libero tempore, cum soluta nobis est eligendi."

"Temporibus autem quibusdam et aut officiis debitis!"